With the planet in the midst of a global pandemic I’ve pretty much stayed away from blogging about politics, despite being sorely temped to vent my spleen at the populist stupidity on display in countries like the USA, Brazil and of course (to a lesser extent) the UK. I’ve also avoided talking about the looming deadline of Brexit. Well, haven’t most people? Their attentions have been elsewhere. The problem is, whilst everyone’s been looking elsewhere, the clock hasn’t stopped ticking and the Government has made sure of that by its mad insistence that – whatever happens – there will be no extension to the transition period, so on the 1st January 2021 we’re out, deal or no deal.

It’s becoming increasingly likely that ‘no deal’ is exactly what we’ll have…

Of course, the Governments narrative is that will be the fault of an intransigent EU. That narrative will be backed up by the Brexity newspapers like the Mail and the Express, and a lot of people will fall for it, both because they want to – and also because – if Brexit has shown one thing, it’s how ill-informed the majority of the population are about politics in general and the EU in particular.

Here’s a stark warning of what’s about to happen. You won’t find it covered in detail in most of the media – if at all. It makes too uncomfortable reading for some. This is the full text of a speech delivered (over Zoom) to Eurofi, which is a European financial think tank – by Michel Barnier, the EU’s chief Brexit negotiator, yesterday;

“My sincere apologies for not being able to join you in person.

As you may know, we agreed with the UK to intensify our negotiations, starting this week. We do this to give the negotiations every chance of succeeding.

I continue to believe that an agreement is possible.

The EU will work for this.

We will remain calm, pragmatic and determined until the very end.

Because of the new negotiation agenda this week, I have had to reschedule many meetings.

But I wanted to address you this short video message all the same.

These are difficult times.

The coronavirus pandemic has already taken hundreds of thousands of lives around the world.

Global and EU economies have been hit hard.

Amid the uncertain outlook, I understand you would like clarity on the Brexit negotiations and the ongoing process for assessment of equivalences.

So let me tell you briefly where we stand on these two points.

As you know, the key instrument to regulate interactions with the UK financial system will be our equivalence regimes.

These are autonomous, unilateral tools.

And, as such, they are not part of our current negotiations.

I will come back to these in a moment.

Next to this, as part of our negotiations, we are proposing to include, in our future agreement, a chapter on financial services, in line with what we have in other Free Trade Agreements.

Our proposals would give UK operators legal certainty that they would not face discrimination when establishing themselves in the EU.

And the same for EU operators in the UK.

The UK, however, is looking to go much further. I will be blunt: its proposals are unacceptable.

Firstly, they would severely limit the EU’s regulatory and decision-taking autonomy.

For instance:

The UK is seeking to create a legally enforceable regulatory cooperation framework on financial services in our agreement.

It is attempting to frame the EU’s process for withdrawing equivalence decisions; trying to turn our unilateral decisions into co-managed ones.

It wants to limit the scope of the so-called prudential carve-out.

There is no way Member States or the European Parliament would accept this!

Secondly, the UK is trying to keep as many Single Market benefits as it can.

It would like to make it easy to continue to run EU businesses from London, with minimal operations and staff on the continent.

For instance:

It wants almost free reign for service suppliers to fly in and out for short-term stays (‘Mode 4’).

It proposes provisions on the performance of back-office functions that could create a significant risk of circumvention of financial services regulation.

It wants to assimilate British audit firms to European ones to meet ownership and control requirements.

It wants to ban residence requirements for senior managers and boards of directors, to ensure that all essential functions remain in London.

Let me be clear: The UK chose to no longer be a Member State.

It chose to leave the EU Single Market and stop applying our common ecosystem of rules, supervision and enforcement mechanisms.

In particular, it refuses to recognise any role for the European Court of Justice.

These choices have consequences.

The UK cannot keep the benefits of the Single Market without the obligations.

In the EU’s view, our future cooperation should be voluntary and based on trust.

We would like to set up a voluntary framework for dialogue among regulators and supervisors that would allow for intensive exchanges on regulatory and prudential issues.

We already have well-functioning dialogues of this kind with other major financial services jurisdictions.

As for the equivalence assessment process, which is under the responsibility of Executive Vice-President Valdis Dombrovskis and led by experts in DG FISMA:

As you know, the Political Declaration committed us to “best endeavours” to finalise our respective assessments by the end of June.

The European Commission has therefore sent questionnaires to the UK, covering 28 areas where equivalence assessments are possible.

So far, the UK has only answered 4 of these questionnaires.

So we are not there yet.

These assessments are particularly challenging.

Firstly, because they have to be forward-looking, given the UK’s publicly stated intention to diverge from EU rules after 1 January 2021.

Last week, the UK published a paper on its future regulatory framework for financial services.

This is a useful document. We are now analysing it in detail to gain clarity on how UK rules will evolve. But let us have no illusions: The UK will progressively start diverging from the EU framework. This is even one of the main purposes of Brexit.

Secondly, the size of the UK financial market and the very close links between the EU and UK financial systems mean we need to be extra careful.

We need to capture all potential risks: for financial stability, market integrity, investor and consumer protection, and the level playing field.

Ladies and gentlemen,

I know that many of you would like the level and ease of access to our mutual markets to remain the same.

I know that many hope our equivalence decisions will provide continuity.

Many believe that “responsible politicians” on both side of the Channel should make this happen.

But things have to change. The UK and the EU will be two separate markets, two jurisdictions.

And the EU must ensure that important risks to our financial stability are managed within the framework of our Single Market ecosystem of legislation, supervision and jurisdiction.

Having been Commissioner for financial services, I can reassure you that I know well the EU’s capital markets and the role of the UK in some parts of that market. As does Executive Vice-President Dombrovskis.

However – especially in the context of Europe’s economic recovery – we must look beyond short-term adaptation and fragmentation costs, to our long-term interests:

Building our Capital Markets Union. This means strengthening our independence when it comes to financial market infrastructures;

Further deepening the Banking Union and;

Fostering the international role of the euro.

And so, we will only grant equivalences in those areas where it is clearly in the interest of the EU; of our financial stability; our investors and our consumers.

What does this mean in practice?

It means that you need to get ready for 1 January 2021!

We now know that the transition period will not be extended. The EU was open to an extension. But the UK refused. It is the UK’s choice.

So, 1 January 2021 will bring big changes.

UK firms will lose the benefit of the financial services passports.

This should not come as a surprise to you. We have been warning about this for the past 3 years.

Furthermore, as you know well, in some areas – such as insurance, commercial bank lending or deposit-taking – EU law does not provide for the possibility to award equivalences that would grant market access to third-country firms.

In these areas, if British firms want to provide services in the EU, they must ask for an authorisation in the EU. Or comply with all the relevant national regimes of those EU Member States where they want to continue to be active.

Nothing in the agreement that we are negotiating will change this!

These are automatic, mechanical consequences of Brexit.

If you are not yet ready for these broad changes that will take place – whatever happens – on 1 January 2021, I can only urge you to speed up preparations and take all necessary precautionary measures!

I know how mobile and dynamic the financial industry is.

I trust in its capacity to adapt to new times and continue to contribute to developing the Capital Markets Union and Single Market for financial services.

We cannot do this with regulation alone.

You all have a crucial role to play. As of now.

Let us look to the future not with fear of the unknown but with confidence in our well-regulated and supervised markets.

Thank you to all of you for your attention. And thank you, David, Didier for your invitation.

I hope to see you in person next time! ”

To recap one very important point “So, 1 January 2021 will bring big changes.

UK firms will lose the benefit of the financial services passports”.

This is going to be devastating to the UKs financial sector and it didn’t need to happen at all. Instead, it’s about to happen in the midst of a global pandemic, when firms are struggling to cope with the consequences. It is utterly, utterly mad, but it’s solely the British Governments decision and no-one else’s.

Covid 19 has caused the worst contraction to the UK economy in 41 years.

Every day we get news of more companies shutting. Today TM Lewin announced its closing all its UK stores whilst sandwich seller Upper Crust has warned 5,000 jobs could go. Yesterday Airbus announced 1,700 UK jobs will be going. The list is growing every day and Brexit is only going to make that worse. We’re the only economy that’s doing this to itself, no-one else is that stupid.

Still, all these newly unemployed folks will be able to get work abroad, won’t they? Oh, wait, the Home Secretary and Tory backbenchers are taking great delight in announcing that Freedom of Movement is ending on January 1st.

If you ignore the obvious oxymoron in the first sentence, you’ll notice a glaring omission. Freedom of movement is a two way street. The Government is boasting of ending OUR freedom of movement too – and it’s worse. Much worse. The EU 27 know they’ve had their freedom of movement reduced by just one country. We’ve had ours reduced in the opposite direction. We’ve lost it to 26 nations, not 1. Yet many Britons still seem blissfully unaware of what’s about to happen – and don’t even start me on the utter stupidity of retired folk owning homes in countries like Spain and Portugal who voted Leave….

Of course, due to the Government making a mess of handling the pandemic, many thousands of Britons have already had their freedom of movement removed. Permanently.

Despite the richness of the English vernacular there simply aren’t enough expletives to describe the utter shit-show this country has become over these past few years.

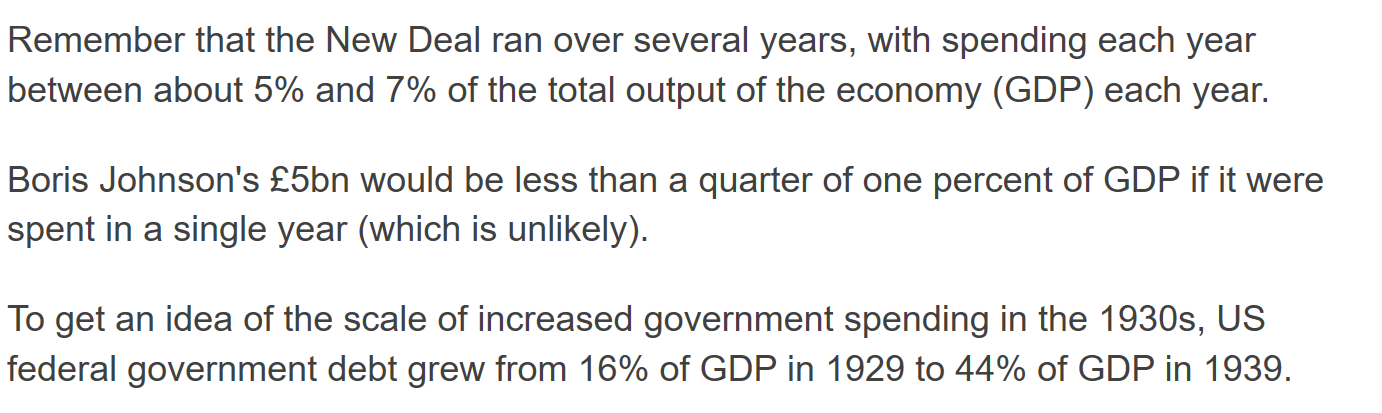

Meanwhile, the political game of “look over there” is played out in Government as Johnson announces his economic ‘new deal’, comparing it to FDR’s new deal in America in the 1930s. In this deception he’s relying on an uncritical media and an ignorant public. Not only is the £5bn he’s announced peanuts in comparison, it’s not even new money. It’s yet more re-announcements of earlier spending commitments. The BBCs ‘Fact Check’ blew the whistle on this here. It makes depressing reading as the scale of Johnson’s con is laid bare. For example…

But the party faithful will lap it up, and it will work as yet another dead cat as the arguments over it detract from the unfolding coronavirus scandal and Brexitshambles until its too late.

How I wish I could get the hell away out of this mess and watch it unfold from somewhere where it had no impact on me. Sadly, we really are caught between a rock and a hard place at the moment. But only one of them is truly of our own making, not that those responsible seem in the slightest bit willing to take responsibility for it. This is like being trapped in a slow motion car crash. You know the result will be awful for all those involved – including yourself – but you are utterly powerless to stop it…

I’ve a favour to ask…

If you enjoy reading this blog, please click on an advert or two. You don’t have to buy anything you don’t want to of course (although if you did find something that tickled your fancy would be fab!), but the revenue from them helps to cover some of the cost of maintaining this site – and right now (because of Covid), us locked-down freelances need all the help that we can get…

Thank you!