Normality has resumed after the New Year holiday. Train services are running as per the usual timetable (with the odd exception) and some of the major investment projects carried out over the holiday period have borne fruit. London Bridge station’s seen the last 5 rebuilt platforms open, The GWML has seen electric train services extended from Reading to Didcot and more works been completed on the EGIP project in Scotland. Oh, and we’ve had the annual fare increase kick-in, which has produced the usual gush of uninformed comment and politicking over railway nationalisation from the Labour party.

What’s lost in this mass of misinformation is the facts around the fare increases. They’re calculated on the basis of the Retail Price Index – which has shot up in the part year due to Brexit and the fall in the pound leading to inflation. Also, let’s not forget that this isn’t ‘profiteering’ by the Train operators, but a rise in fares regulated by the Government. It’s a political decision. In fact, I’m told the unregulated fares (those set by the train operators themselves) have risen by less than the 3.6% regulated fares have.

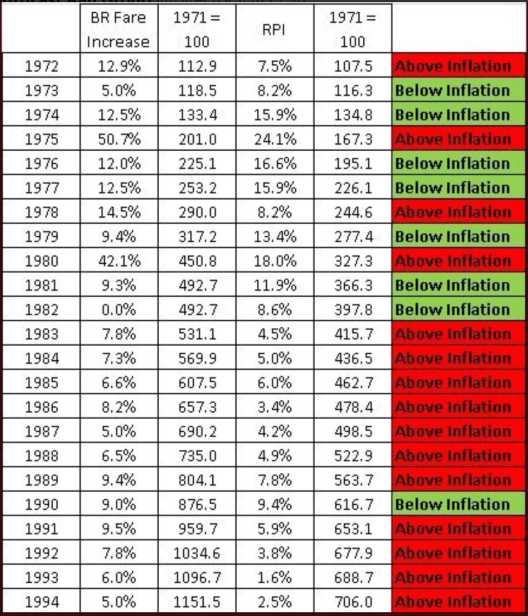

I’ve got to give a hat-tip to @DirectorSERG for supplying this handy little chart which details BR fare increases from 1972 until 1994.

As you can see, the majority were all well above the rate of inflation and there were some eye-watering ones of 50.7% in 1975 and 42.1% in 1980. It’s a rather useful antidote to the rose-tinted views of some that BR = good, Privatisation = bad. Quite how nationalisation is meant to cut rail fares whilst guaranteeing the levels of investment we’re seeing in the railways is a question Labour don’t seem too keen on answering.

Meanwhile, it’s worth remembering that the TOC’s aren’t exactly ‘fat cats’. Their margins are around 3%, which compares very favourably with other state-owned railways like the Netherlands, which would expect a 7% return.

It has been noted that when Arriva took over Northern the Brigg Line fares came down between £2 to £3.

The fares have now risen between 30-50p due to the government increases who say this is going towards service improvements, Brigg Line trains will still run a 1 day a week service.